Parametric insurance pays within days after an Earthquake

EARTHQUAKE

RAPID RECOVERY INSURANCE

The parametric Earthquake Rapid Recovery Insurance (ERRI) provides loss payments to policy holders after a devastating earthquake to secure livelihood or to keep business running within days.

The loss payment is defined by the maximum Earthquake Peak Ground Acceleration (PGA) intensity reported at the Insured Location. The Insured Location is one or multiple circles with a radius in miles around the Insured Address.

In the trigger event, based on the data from the United States Geological Survey (USGS), the loss payment is wired to the policyholder’s bank account within days.

KEY SELLING POINTS

° No proof of physical loss to your property

° No proof of loss to Business Income

° Wire transfer of loss payment within days

directly to the Insured

° Loss trigger based on data from the United

States Geological Survey (USGS)

° Transparent product administrated through

best-in-class platform solution

° Backed by reputable reinsurer

ERRI PRODUCT

The product is designed as parametric insurance where the Insured Location is a circle with a defined radius around the Insured Address.

The Insured receives a payout within days when a earthquake is reported in the Insured Location in a relevant category.

The ERRI Event Coverage Table describes the payout amount per Earthquake Peak Ground Accceleration (PGA) Category in the Insured Location. There may be multiple payouts during the Policy Period, howe- ver the maximum payout is capped at the Sum Insured.

ERRI EVENT COVERAGE TABLE

If an Earthquake is reported in the Insured Location, loss payments are due based on the Event Coverage Table.

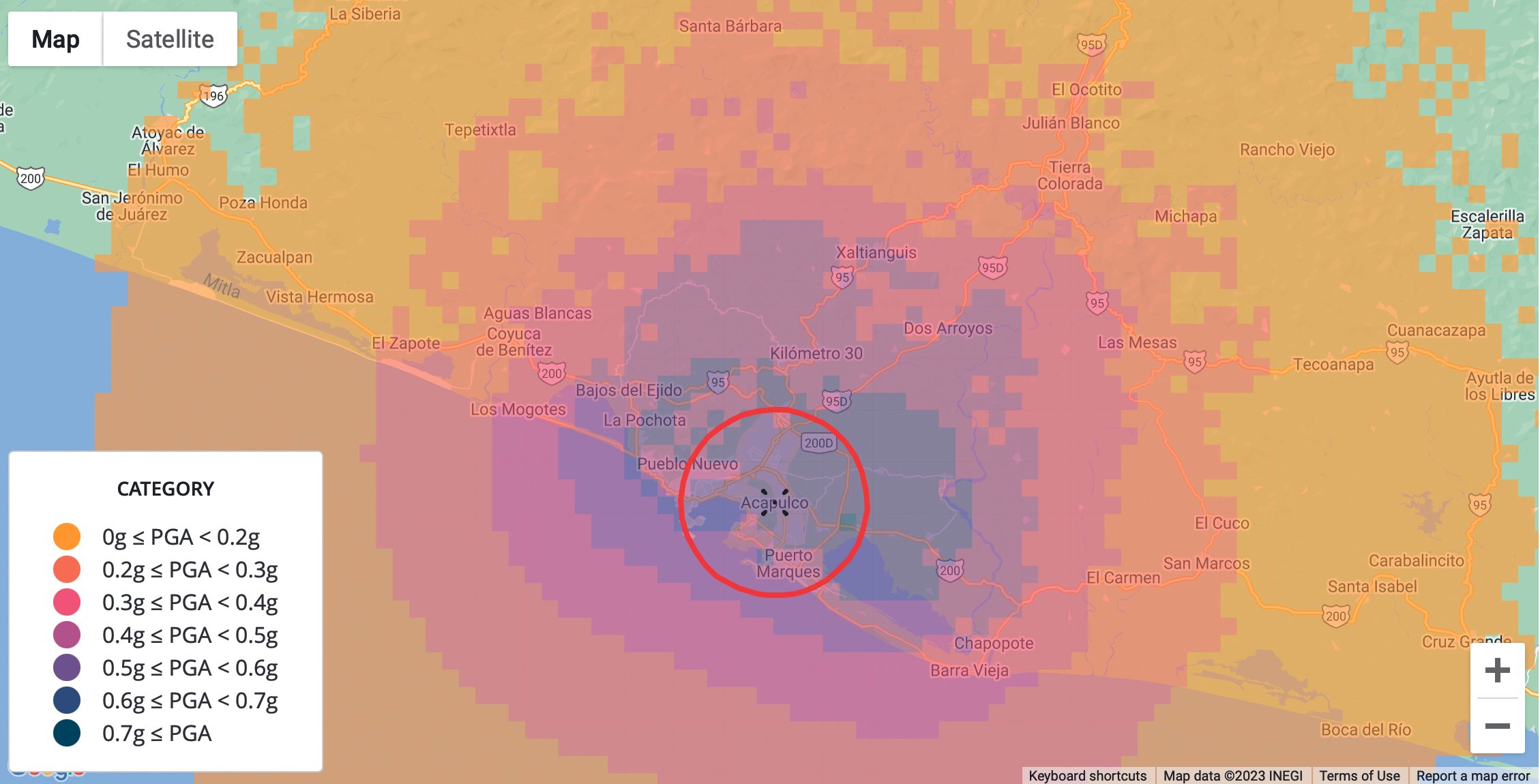

HOW IT IS MEASURED

The USGS publishes PGA Shake Maps after significant earthquakes. The Shake Maps report ground motion for Grid Points in the region affected by the Earthquake.

The relevant earthquake category is determined based on the highest PGA value reported for grid points in the Insured Location per Earthquake Cluster. Only the Grid Points which are located in the Insured Location are considered.

ERRI POLICY TERMS EXAMPLE

PAYOUT EXAMPLES

Scenario 1

A shop owner in Manzanillo purchased an ERRI with a Policy Limit of $1,000,000. The Insured Location is a circle with a 10 km radius around the shop. The October 1995 Earthquake was an Eligible Event.

The maximum PGA value reported in the Insured Location was in the 0.6g-0.7g Category. The shop owner received a $ 600,0000 payout.

Scenario 2

A factory in Atlixco purchased an ERRI with a Policy Limit of $1,000,000. The Insured Location is a circle with a 10 km radius and around the factory. The September 2017 Earthquake was an Eligible Event.

The maximum PGA value reported in the Insured Location was in the 0.4g-0.5g Category. The factory owner received a $150,000 payout.

Scenario 3

A business owner in New Zealand purchased a FRRI for 2023 with a Policy Limit of $200,000.

The Insured Location is a circle with a 25km radius around the Insured Address.

Cyclone Gabrielle triggered rainfall of 150mm or the 10 – 25 year return period at one grid cell within the Insured Location. The business owner received a $50,000 payout.